by Scott Martindale

by Scott Martindale

President & CEO, Sabrient Systems LLC

July saw new highs for the broad market indexes followed by a big fall from grace among the Magnificent Seven (MAG-7) stocks. But it looked more like a healthy rotation than a flight to safety, with a broadening into neglected market segments, as inflation and unemployment metrics engendered optimism about a dovish policy pivot from the Federal Reserve. The rotation of capital within the stock market—as opposed to capital flight out of stocks—kept overall market volatility modest. But then along came the notorious month of August. Is this an ominous sign that the AI hype will come crashing down as the economy goes into a recession? Or is this simply a 2023 redux—another “summer sales event” on stock prices—with rate cuts, accelerating earnings, and new highs ahead? Let’s explore the volatility spike, the reset on valuations, inflation trends, Fed policy, and whether this is a buying opportunity.

Summary

Up until this month, a pleasant and complacent trading climate had been in place essentially since the Federal Reserve announced in Q4 2023 its intended policy pivot, with a forecast of at least three rate cuts. But August is notorious for its volatility, largely from instability on the trading floor due to Wall Street vacations and exacerbated by algorithmic (computer-based) trading systems. In my early-July post, I wrote that I expected perhaps a 10% correction this summer and added, “the technicals have become extremely overbought [with] a lot of potential downside if momentum gets a head of steam and the algo traders turn bearish.” In other words, the more extreme the divergence and euphoria, the harsher the correction.

Indeed, last Monday 8/5 saw the worst one-day selloff since the March 2020 pandemic lockdown. From its all-time high on 7/16 to the intraday low on Monday 8/5 the S&P 500 (SPY) fell -9.7%, and the Technology Select Sector SPDR (XLK) was down as much as -20% from its 7/11 high. The CBOE Volatility Index (VIX) hit a colossal 67.73 at its intraday peak (although tradable VIX futures never came close to such extremes). It was officially the VIX’s third highest reading ever, after the financial crisis in 2008 and pandemic lockdown in 2020. But were the circumstances this time around truly as dire as those two previous instances? Regardless, it illustrates the inherent risk created by such narrow leadership, extreme industry divergences, and high leverage bred from persistent complacency (including leveraged short volatility and the new zero-day expiry options).

The selloff likely was ignited by the convergence of several issues, including weakening economic data and new fears of recession, a concern that the AI hype isn’t living up to its promise quite fast enough, and a cautious Fed that many now believe is “behind the curve” and making a policy mistake by not cutting rates. (Note: I have been sounding the alarm on this for months.) But it might have been Japan at the epicenter of this financial earthquake when the Bank of Japan (BoJ) suddenly hiked its key policy rate and sounded a hawkish tone, igniting a “reverse carry trade” and rapid deleveraging. I explain this further in today’s post.

Regardless, by week’s end, it looked like a non-event as the S&P 500 and Nasdaq 100 clawed back all their losses from the Monday morning collapse. So, was that it for the summer correction? Are we all good now? I would say no. A lot of traders were burned, and it seems there is more work for bulls to do to prove a bottom was established. Although the extraordinary spike in fear and “blood in the streets” was fleeting, the quick bounce was not convincing, and the monthly charts look toppy—much like last summer. In fact, as I discuss in today’s post, the market looks a lot like last year, which suggests the weakness could potentially last into October. As DataTrek opined, “Investor confidence in the macro backdrop was way too high and it may take weeks to fully correct this imbalance.”

Stock prices are always forward-looking and speculative with respect to expectations of economic growth, corporate earnings, and interest rates. The FOMC held off on a rate cut at its July meeting even though inflation is receding and recessionary signals are growing, including weakening economic indicators (at home and abroad) and rising unemployment (now at 4.3%, after rising for the fourth straight month). Moreover, the Fed must consider the cost of surging debt and the impact of tight monetary policy and a strong dollar on our trading partners. On the bright side, the Fed no longer sees the labor market as a source of higher inflation. As Fed Chair Jerome Powell said, “The downside risks to the employment mandate are now real.”

The real-time, blockchain-based Truflation metric (which historically presages CPI) keeps falling and recently hit yet another 52-week low at just 1.38%; Core PCE ex-shelter is already below 2.5%; and the Fed’s preferred Core PCE metric will likely show it is below 2.5% as well. So, with inflation less a worry than warranted and with corporate earnings at risk from the economic slowdown, the Fed now finds itself having to start an easing cycle with the urgency of staving off recession rather than a more comfortable “normalization” objective within a sound economy. As Chicago Fed president Austan Goolsbee said, “You only want to stay this restrictive for as long as you have to, and this doesn’t look like an overheating economy to me.”

The Fed will be the last major central bank in the West to launch an easing cycle. I have been on record for months that the Fed is behind the curve, as collapsing market yields have signaled (with the 10-year Treasury note yield falling over 80 bp from its 5/29 high before bouncing). It had all the justification it needed for a 25-bp rate cut at the July FOMC meeting, and I think passing on it was a missed opportunity to calm global markets, weaken the dollar, avert a global currency crisis, and relieve some of the burden on highly indebted federal government, consumers, businesses, and the global economy. Indeed, I believe Fed inaction forced the BoJ rate hike and the sudden surge in US recession fears, leading to last week’s extreme stock market weakness (and global contagion).

In my view, a terminal fed funds “neutral” rate of 3.0-3.5% (roughly 200 bps below the current “effective” rate of 5.33%) seems appropriate. Fortunately, today’s lofty rate means the Fed has plenty of potential rate cuts in its holster to support the economy while still remaining relatively restrictive in its inflation fight. And as long as the trend in global liquidity is upward, then the risk of a major market crash this year is low, in my view. Even though the Fed has kept rates “higher for longer” throughout this waiting game on inflation, it has also maintained liquidity in the financial system, which of course is the lifeblood of economic growth and risk assets. Witness that, although corporate credit spreads surged during the selloff and market turmoil (especially high yield spreads), they stayed well below historical levels and fell back quickly by the end of the week.

So, I believe this selloff, even if further downside is likely, should be considered a welcome buying opportunity for long-term investors, especially for those who thought they had missed the boat on stocks this year. This assumes that the proverbial “Fed Put” is indeed back in play, i.e., a willingness to intervene to support markets (like a protective put option) through asset purchases to reduce interest rates and inject liquidity (aka quantitative easing). The Fed Put also serves to reduce the term premium on bonds as investors are more willing to hold longer-duration securities.

Longer term, however, is a different story, as our massive federal debt and rampant deficit spending is not only unsustainable but potentially catastrophic for the global economy. The process of digging out of this enormous hole will require sustained, solid, organic economic growth (supported by lower tax rates), modest inflation (to devalue the debt without crippling consumers), and smaller government (restraint on government spending and “red tape”), in my view, as I discuss in today’s post.

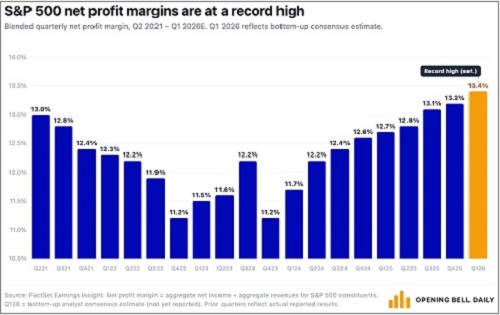

In buying the dip, the popular Big Tech stocks got creamed. However, this served to bring down their valuations somewhat, their capital expenditures and earnings growth remains robust, and hedge funds are generally underweight Tech, so this “revaluation” could bode well for a broader group of Tech stocks for the balance of the year. Rather than rushing back into the MAG-7, I would suggest targeting high-quality, fundamentally strong stocks across all market caps that display consistent, reliable, and accelerating sales and earnings growth, positive revisions to Wall Street analysts’ consensus estimates, rising profit margins and free cash flow, solid earnings quality, and low debt burden. These are the factors Sabrient employs in selecting our growth-oriented Baker’s Dozen, value-oriented Forward Looking Value (which just launched on 7/31), growth & income-oriented Dividend portfolio, and the Small Cap Growth (an alpha-seeking alternative to a passive position in the Russell 2000).

We also use many of those factors in our SectorCast ETF ranking model. And notably, our Earnings Quality Rank (EQR) is a key factor in each of these models, and it is also licensed to the actively managed, absolute-return-oriented First Trust Long-Short ETF (FTLS) as an initial screen.

Each of our alpha factors and their usage within Sabrient’s Growth, Value, Dividend income, and Small Cap investing strategies is discussed in detail in Sabrient founder David Brown’s new book, How to Build High Performance Stock Portfolios, which will be published this month (I will send out a notification).

Click here to continue reading my full commentary, in which I go into greater detail on the economy, inflation, monetary policy, valuations, and Sabrient’s latest fundamental-based SectorCast quantitative rankings of the ten U.S. business sectors, current positioning of our sector rotation model, and several top-ranked ETF ideas. Also, here is a link to this post in printable PDF format. I invite you to share it as appropriate (to the extent compliance allows). You also can sign up for email delivery of this periodic newsletter at Sabrient.com.