by Scott Martindale

by Scott Martindale

President & CEO, Sabrient Systems LLC

Given the latest inflation reports last week and this week’s FOMC meeting, I thought I would offer up some perspective today in a short post. Although there are plenty of other issues to worry about, including the historic auto workers’ strike and an impending federal government shutdown, all eyes are focused on the Fed’s reaction to inflation and jobs reports in the form of monetary policy, specifically interest rates and money supply.

The 2-year yield again has been battling the important 5% threshold, which I have called a “line in the sand” for stocks. After challenging the March and July highs above 5% during August, it had appeared to me that it was just another buyable bond selloff, driven by the various reasons I discussed in my 9/1/2023 post. Indeed, yields pulled back substantially to end the month of August, as both bond and stock prices rose. But this month’s renewed weakness in bonds (and the rise in yields) suggests a “buyer’s strike” as investors generally have been moving to cash ahead of this week’s FOMC meeting. At the moment, resistance at the 5-handle seems to have given way, with the rate now at 5.10% as I write (and stocks are weak).

To be sure, last week’s inflation reports gave mixed signals. CPI and PPI both ticked up from their June lows of 3.0% and 0.1%, respectively, to August readings of 3.7% and 1.6%, which appear troubling to the Fed’s ongoing inflation fight. Certainly, the recent surge in oil prices to above $90 has hurt the cause, as has the stubborn shelter cost component, which makes up 42% of CPI. In addition, Mexico’s rise as a “near-shore” manufacturing hub for the US, its extreme wage inflation, and the extraordinary strength of the peso has increased prices of its exports to the US.

On the other hand, rising oil prices are like a tax on consumers, limiting their disposable income to buy other things. Same with the imminent student loan payment restart. Also, core rates (ex-food and energy) for CPI and PPI both fell to 4.3% and 2.2%, respectively. And given the emerging “lag effects” of rising interest rates on rents and owner’s equivalent rent (OER), many economists expect shelter costs to begin to decline very soon. Indeed, by Q4 2024, JPMorgan chief global strategist David Kelly expects both headline and core PCE to fall below the Fed’s 2% target and perhaps hit 1.5%, largely driven by declines in shelter costs, new and used car prices, auto insurance, and car maintenance.

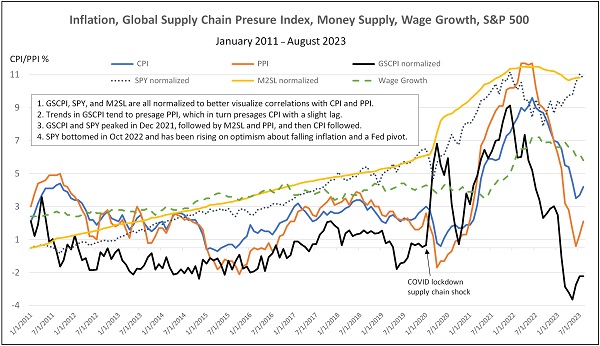

Below is an updated version of a chart I present from time to time. It compares trends in CPI and PPI versus the New York Fed’s Global Supply Chain Pressure Index (GSCPI), which measures the number of standard deviations from the historical average value. It also shows wage growth, M2 money supply (M2SL), and the S&P 500 (SPY). I know the chart is busy, but it tells a good story.

Read on....