by Scott Martindale

by Scott Martindale

President & CEO, Sabrient Systems LLC

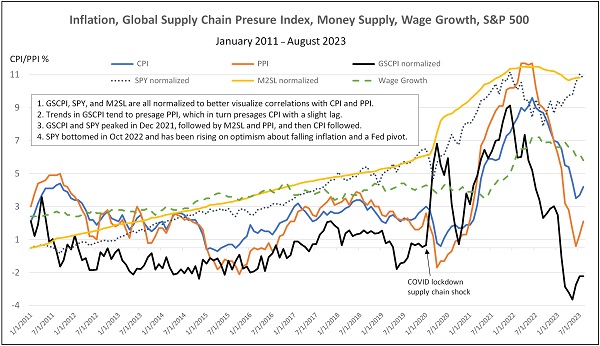

Stocks and bonds both sold off in August before finishing the month with a flourish, as signs that the jobs market is weakening suggest an end to Fed rate hikes is nigh. The summer correction in equities was entirely expected after the market’s extraordinary display of strength for the first seven months of the year in the face of a relentlessly hawkish Federal Reserve, even as CPI and PPI have fallen precipitously. State Street’s Institutional Investor Risk Appetite Indicator moved dramatically from bearish in May to highly bullish at the end of July, and technical conditions were overbought. And although the depth of the correction took the bulls by surprise, it was quite orderly with the CBOE Volatility Index (VIX) staying tame (i.e., never even approaching the 20 handle). In fact, a 5% pullback in the S&P 500 is not unusual given the robust 20% YTD return it had attained in those seven months. Weakness in bonds, gold, and commodity prices also reversed.

Moreover, IG, BBB, and HY bond spreads have barely moved during this market pullback despite rising real rates, which signals that the correction in stocks is more about valuations in the face of the sudden spike in interest rates (and fears of “higher for longer”) rather than the health of the economy, earnings, or fundamentals. Certainly, the US economy looks much stronger than any of our trading partners (which Fed chair Powell seems none too happy about), with the Atlanta Fed’s GDPNow model estimating a robust 5.6% growth for Q3 (as of 8/31) and the dollar surging in a flight to safety [in fact, the US Dollar Index Fund (UUP) recently hit a 2023 high].

However, keep in mind that the US is not an island unto itself but part of a complex global economy and thus not immune to contagion, so the GDP growth rate will likely come down. Moreover, Powell said in his Jackson Hole speech that the Fed’s job is “complicated by uncertainty about the duration of the lags with which monetary tightening affects economic activity and especially inflation.”

Investors have generally retained their enthusiasm about stocks despite elevated valuations, rising real interest rates (creating a long-lost viable alternative to stocks—and a poor climate for gold), a miniscule equity risk premium, and a Fed seemingly hell-bent on inducing recession in order to crush sticky core inflation. Perhaps stock investors have been emboldened by the unstoppable secular force of artificial intelligence (AI) and its immediate benefits to productivity and profitability (not just “hope”)—as evidenced by Nvidia’s (NVDA) incredible earnings release last week.

I have discussed in recent posts about how the Bull case seems to outweigh the (highly credible) Bear case. However, the key tenets of the Bull case—and avoidance of recession—include a stable China. Since 2015, I have been talking about a key risk to the global economy being the so-called “China Miracle” gradually being exposed as a House of Cards, and perhaps never before has it seemed so close to implosion, as it tests the limits of debt-fueled growth—and a creeping desperation coupled with an inability (or unwillingness) to pivot sharply from its longstanding policies makes it even more dangerous. I talk more about this in today’s post.

Yet despite all the significant challenges and uncertainties, I still believe stocks are in a normal/predictable summer consolidation—particularly after this year’s surprisingly strong market performance through July—with more upside to come. My only caveat has been that the 2-year Treasury yield needs to remain below 5%—a critical “line in the sand,” so to speak. Although I (and many others) often cite the 10-year yield because of its link to mortgage rates, I think the 2-year is important because it reflects a broad expectation of inflation and the duration of the Fed’s “higher for longer” policy. Notably, during this latest spike in rates, the 2-year again eclipsed that critical 5-handle for the third time this year and challenged the 7/5 intraday high of 5.12%, before pulling back sharply to close the month below 4.9%.

If the 2-year reverses again and surges to new highs, I think it threatens a greater impact on our economy (as well as our trading partners’) as businesses, consumers, and governments manage their maturing lower-rate debt—and ultimately impacts the housing market and risk assets, like stocks. But instead, I see it as just another short-term rate spike like we saw in March and July, as investors sort out the issues described in my full post below. Indeed, August finished with a big fall in rates in concert with a big jump in stocks, gold, crypto, and other risk assets across the board, as cracks in the jobs and housing markets are showing up, leading to a growing belief that the Fed is finished with its rate hikes—as I think they should be, particularly given the resumption of disinflationary secular trends and a deflationary impulse from China.

Some economists believe that extreme stock valuations and the ultra-low equity risk premium are pricing in both rising earnings and falling rates—an unlikely duo, in their view, on the belief that a strong economy is inherently inflationary while a weakening economy suggests lower earnings—and thus, recession is inevitable. But I disagree. For one, respected economist Ed Yardeni has observed that we have already been in the midst of a “rolling recession” across segments of the economy that is now turning into a “rolling expansion.” And regarding elevated valuations in the major indexes, my observation is that they are primarily driven by a handful of mega-cap Tech names. Minus those, valuations across the broader market are much more reasonable, as I discuss in today’s post.

Indeed, rather than passive positions in the broad market indexes, investors may be better served by strategies that seek to exploit improving market breadth and the performance dispersion among individual stocks. Sabrient’s portfolios include Baker’s Dozen, Forward Looking Value, Small Cap Growth, and Dividend, each of which provides exposure to market segments and individual companies that our models suggest may outperform. Let me know how I can better serve your needs, including speaking at your events (whether by video or in person).

As stocks and other risk assets finish what was once destined to be a dismal month with a show of renewed bullish conviction, allow me to step through in greater detail some of the key variables that will impact the market through year-end and beyond, including the economy, valuations, inflation, Fed policy, the dollar, and China…and why I remain bullish. I also review Sabrient’s latest fundamentals based SectorCast quant rankings of the ten U.S. business sectors (topped by Technology and Energy) and serve up some actionable ETF trading ideas.

Click here to continue reading my full commentary … or if you prefer, here is a link to my full post in printable PDF format (as some of my readers have requested).