Demystifying Absolute Return Stock Trading Strategies

You’ve heard it before: trading today’s stock market can be hazardous to both your wealth and health. The market can go up fast…and it can fall even faster. In such an environment, many sophisticated investors and portfolio managers turn to “absolute return” strategies that seek to make money no matter where the market goes.

But this concept can be intimidating to experienced and newbie traders alike. Let me demystify the concept and show how any investor can incorporate an absolute return approach—no matter what their experience level or account size.

Before we go any further, let’s review the concept of risk.

Sources of Risk

Risk is a scary word to investors, but the reality is that you can’t make any kind of meaningful return without taking on some risk. The there are two kinds of risk that we deal with in the stock market: systematic and unsystematic.

Unsystematic risk is company or industry-specific risk. It is also known as specific, diversifiable, or residual risk. It can be reduced through diversification. The impact from a bad news event, an earnings miss, or an analyst downgrade is considered unsystematic risk.

But even a portfolio of well-diversified assets cannot escape risk. Systematic risk is also known as market risk or un-diversifiable risk. It represents the risk inherent to the entire market or an entire market segment. The impact from things like global recession, war, terrorism, or inflation cannot be reduced or controlled through diversification, but it can be addressed through hedging.

Limiting Risk

The first way we limit risk in an absolute return strategy is to diversify by buying “baskets” of longs and shorts from various market segments, so that one or two blow-ups won’t crater your entire portfolio. This reduces the unsystematic or diversifiable risk. In Sabrient’s models, we usually strive for 10 to 50 positions, with limitations on the number of positions coming from each sector and/or industry. Most investors are comfortable with the concept of diversification.

However, for systematic or market risk, it can only be addressed by hedging—which means holding short positions.

At this point, the concept of shorting a stock stops many investors in their tracks, particularly those with less experience or smaller accounts.

And rightly so, because there is no limit to the amount you can lose if you sell short a stock that you don’t own…and hold it as it rises to the stratosphere. In addition, the process of short selling can be intimidating or difficult, such as if you broker doesn’t have the shares available for you to borrow.

But there are other ways to play the short side if you don’t have the appetite or account size for shorting.

The most popular alternative to shorting stocks is to buy put options on those same stocks, or to buy puts on an overall market index or sector exchange-traded fund (ETF). The vast majority of the more liquid stocks are optionable, and your risk is limited to the premium (i.e., purchase price) paid.

You can do this on the long side, too, by purchasing call options. Options limit your risk to the premium paid—but of course they are an expiring asset whose price includes a “time premium.” so they suffer from time premium erosion. (There is no free lunch.)

Absolute Return as a Portfolio Strategy

What does absolute return mean? It is the actual return that an asset or portfolio of assets achieves over time, without regard to how it performs relative to a benchmark (i.e., relative return).

A typical example of relative return is a long-only mutual fund that seeks to outperform a market index, fund category, or its peers. On the other hand, an absolute return strategy strives for positive absolute returns in all market conditions, whether the market goes up or down—usually by employing some form of “market neutral” approach, including short selling, futures, options, leverage. The resulting portfolio generally will show low correlation with the overall market performance.

In a nutshell, an absolute return strategy seeks to make money whether the market goes up or down. In fact, even if the overall market stays flat, you might still make money on the relative performance of your selection of stocks.

Hedge funds can get quite analytical about their market neutral implementation, rebalancing constantly to maintain a “beta zero” position (note that correlation with the market would be a beta of 1.0, and inverse correlation is -1.0). However, many portfolio managers or traders simply strive for a “dollar neutral” portfolio allocation, with approximately equal capital allocated between their longs and shorts.

So, you would need to own, or otherwise be positioned to benefit from an increase in price in, a given basket of stocks (“longs”) and at the same time be positioned to benefit from a decline in price of a separate basket of stocks (“shorts”). You are simply seeking to capture the performance spread between the longs and shorts.

Example of an Absolute Return Long/Short Strategy

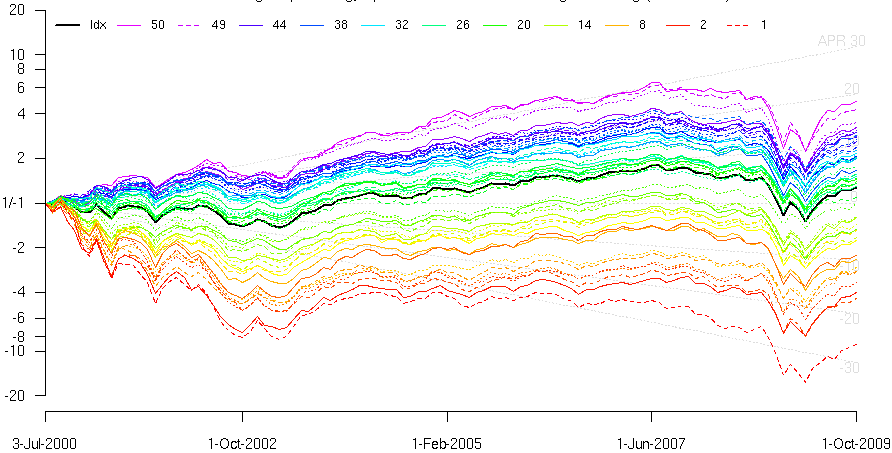

Below is a performance chart of a rank that is ideal for absolute return long/short strategies. It scores stocks based on growth potential, valuation, and earnings quality. Each curve represents the performance of the given quantile of the eligible universe. There are 50 curves shown, so for an eligible universe of 2000 stocks, quantile 1 represents the compounded performance of the highest scoring 40 stocks, re-scored and rebalanced every month for 9 years. Quantile 2 is the second highest-scoring 40 stocks…on down to quantile 50 at the bottom. What this tells us is that over time, the highest-scoring stocks in quantile 1 will tend to greatly outperform the lowest-scoring stocks.

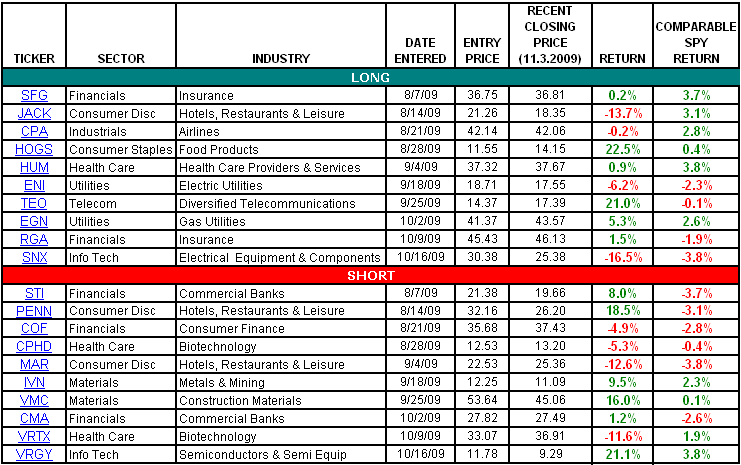

Below is an example of a 10 long / 10 short portfolio for an absolute return portfolio based on the ranking system shown above. In this sample portfolio, one new long & short are put on each week as a form of a pairs trade. Also shown is what a comparable investment in the S&P 500 SPDR (SPY) would have returned (long or short).

You can see that sometimes the given long or short outperforms the SPY long or short position and sometimes it doesn’t. But as illustrated in the previous chart, over time the long positions tend to outperform the averages…and greatly outperform the short positions.

If we look at each week’s positions as a long/short pair in which we are seeking to capture the performance spread between the long & short, we find that 7 of the 10 paired positions in the sample table provided a positive net long/short return, averaging +5.5% per paired position, versus the SPY average return of less than +0.9% per long trade.

Best of all was the 9/25/09 set of positions in which the TEO long went up +21%, and the VMC short went up +16%, for 5-week total return of +37% (assuming shorts margined against all-cash longs). That’s the ideal outcome!

Summary – A Strategy for All Seasons

Even the most experienced investors and traders can get caught up worrying about risk. It can make it difficult to sleep at night when the market is in turmoil and you have a lot of your money invested. One way to deal with this uncomfortable situation is to invest in an all-weather absolute return long/short portfolio strategy that seeks to make money no matter where the stock market may be headed by capturing the performance spread between a basket of long and short positions.

Thus, unsystematic company-specific risk is reduced by trading diversified baskets of stocks, and systematic market risk is controlled using hedges or a market neutral approach—employing short positions or put options.

Although short selling within an absolute return portfolio strategy can be an intimidating endeavor, holding a diversified basket of shorts or employing alternative put options are effective ways of gaining short exposure while reducing the risk associated with selling short an individual stock. The most important concept is to use a proven system for choosing your positions—and stick with it. You’ll sleep like a baby.